Cyber liability is no longer an option for businesses—it’s a necessity. With the rise of cybercrime targeting small businesses, it’s vital to have the right protection in place. But here’s the big question many business owners face: Should you invest in a stand-alone cyber liability policy or add an endorsement to an existing policy?

Both options have benefits, and the right choice depends on your business's unique needs. Let's explore the pros and cons of each option and help you determine which is best for your organization.

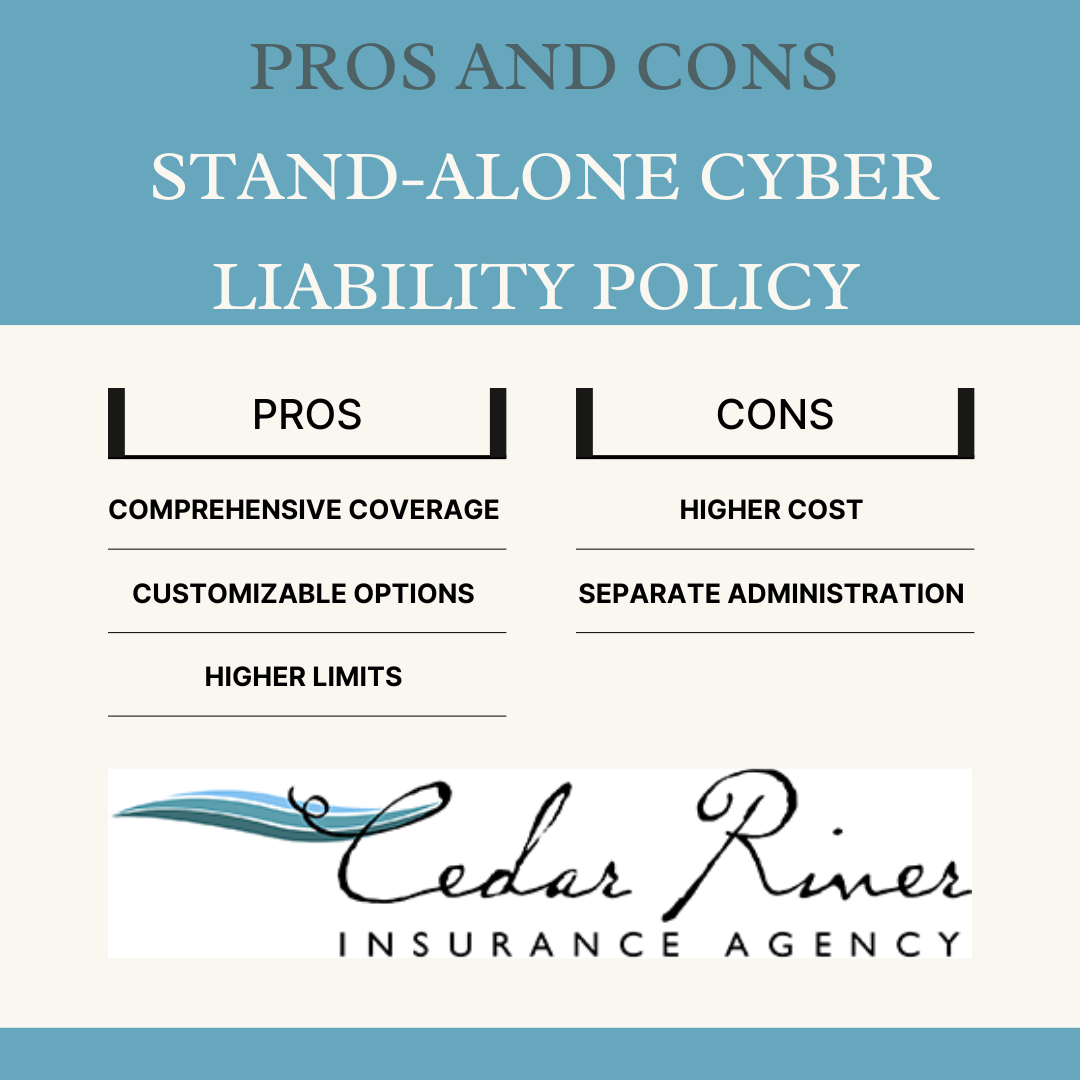

Stand-Alone Cyber Liability Policy vs. Endorsement to an Existing Policy

Stand-Alone Cyber Policy

A stand-alone cyber policy is a dedicated insurance product that exclusively covers cyber risks. These policies are designed to provide robust and customizable coverage against the complex and evolving nature of cybersecurity threats.

Pros of a Stand-Alone Cyber Liability Policy

-

Comprehensive Coverage

Stand-alone policies typically offer broader coverage for issues like data breaches, ransomware attacks, business interruption, and even third-party claims.

-

Customizable Options

Tailor your policy to address your business’s specific risks. For example, if you handle sensitive client data, you can prioritize coverage for data restoration and notification costs.

-

Higher Limits

These policies provide higher coverage limits compared to endorsements, making them ideal for businesses with high exposure to cyber risks.

Cons of a Stand-Alone Cyber Liability Policy

-

Higher Cost

Stand-alone policies can be more expensive than adding an endorsement to your existing policy.

-

Separate Administration

Managing multiple insurance policies requires more attention and organization.

Adding a Cyber Liability Endorsement

An insurance endorsement is a rider added to an existing policy, such as a general liability or business owner policy (BOP), to extend coverage for cyber risks.

Pros of Adding a Cyber Liability Endorsement

-

Cost-Effective

Adding cyber liability as an endorsement is often cheaper than purchasing a stand-alone policy. For small businesses with limited risk exposure, this can be a budget-friendly option.

-

Convenience

Bundling your coverage into one policy makes management and renewals simpler for your business.

Cons of Adding a Cyber Liability Endorsement

-

Limited Coverage

Endorsements typically offer limited coverage, which may not be adequate for larger risks like ransomware or extensive third-party liabilities.

-

Standardized Options

Few opportunities to customize the policy to reflect your specific business needs.

Why Your Business Needs Cyber Liability Coverage

62% of small businesses experienced a cyberattack in the past year. With increasing reliance on technology, even small businesses are vulnerable to cyber threats. Without proper coverage, the fallout from a single data breach can be devastating. Here’s what you’re protecting against with a cyber liability policy:

-

Legal Costs: Cover attorney fees or settlements if you're facing lawsuits due to a breach.

-

Business Interruption: Safeguard your revenue when a cyberattack disrupts operations.

-

Notification Costs: Meet legal obligations to notify customers after a data breach.

-

Reputation Protection: Handle public relations crises and rebuild customer trust.

According to Astra, a leading company providing online security, there are 2,200 cyber attacks per day, with a cyber attack happening every 39 seconds on average. (In the United States.)

Related: Do Small Businesses Need Cyber Insurance if They Practice Good Cyber Hygiene?

What Happens When a Business Lacks Cyber Liability?

To understand the importance of cyber liability insurance, consider these real-world scenarios:

A Ransomware Attack

A small accounting firm’s system was locked by ransomware. A $50,000 payment was demanded to regain access. Without insurance, the business had to pay out of pocket to negotiate and restore its systems, incurring major financial losses.

A Data Breach

A local retailer’s payment system was hacked, exposing customer credit card information. The business faced lawsuits, regulatory fines, and significant reputational damage. With no cyber policy, they had to cover all of the costs themselves.

Email Phishing Scams

A nonprofit organization accidentally transferred $100,000 to a fraudulent account after a phishing attack. A cyber liability policy could have reimbursed these funds and assisted with recovery efforts.

These examples highlight how expensive and disruptive cyber incidents can be—even for small businesses. The financial and reputational risks often far outweigh the cost of robust cyber liability insurance.

Related: Doesn’t My Current Business Insurance Include Cyber Attacks?

Choosing Cyber Liability Based on Your Business Needs

Every business is exposed to unique cyber risks, and the level of coverage you require will largely depend on what type of business you run.

Small Professional Services (Accounting, Legal, Consulting)

High exposure to sensitive client information calls for stand-alone policies that include strong data breach and notification coverage.

Retail and E-Commerce

Due to the handling of payment data, these businesses should prioritize third-party coverage for lawsuits and business interruption coverage in case of online storefront downtime.

Nonprofits and Educational Institutions

A cost-effective cyber endorsement may suit smaller nonprofits, but those with large donor databases or online platforms should consider stand-alone policies.

Manufacturing and Logistics

Cyberattacks targeting supply chain operations can cause significant downtime. Look for policies with business interruption and ransomware negotiation coverage.

Protect Your Business with Cedar River Insurance

Whether you need a stand-alone cyber policy to secure comprehensive coverage or an endorsement to fit into your existing policy, we’ve got you covered. At Cedar River Insurance, we specialize in pairing businesses like yours with the perfect cyber liability solutions.

Want to learn more about your options?

Contact our team at Cedar River Insurance today! Simply call us at 517-580-3819 or request a quick online quote. We’ll help ensure your small business is protected, giving you peace of mind to focus on growing your success.

Don’t leave your business exposed—get the coverage you need now!